Brooklyn Mirage Bankruptcy: When the Trustee Gets Paid First

Inside Avant Gardner's Chapter 11 liquidating trust, Joshua Nahas collects $15K/mo while unsecured creditors wait years for recovery. What happened to "for the benefit of creditors"?

updated on Feb 10,2026

words by Nina K.Malik

Brooklyn Mirage. Mayan Warrior May 2024. Photo by Erik Lorch

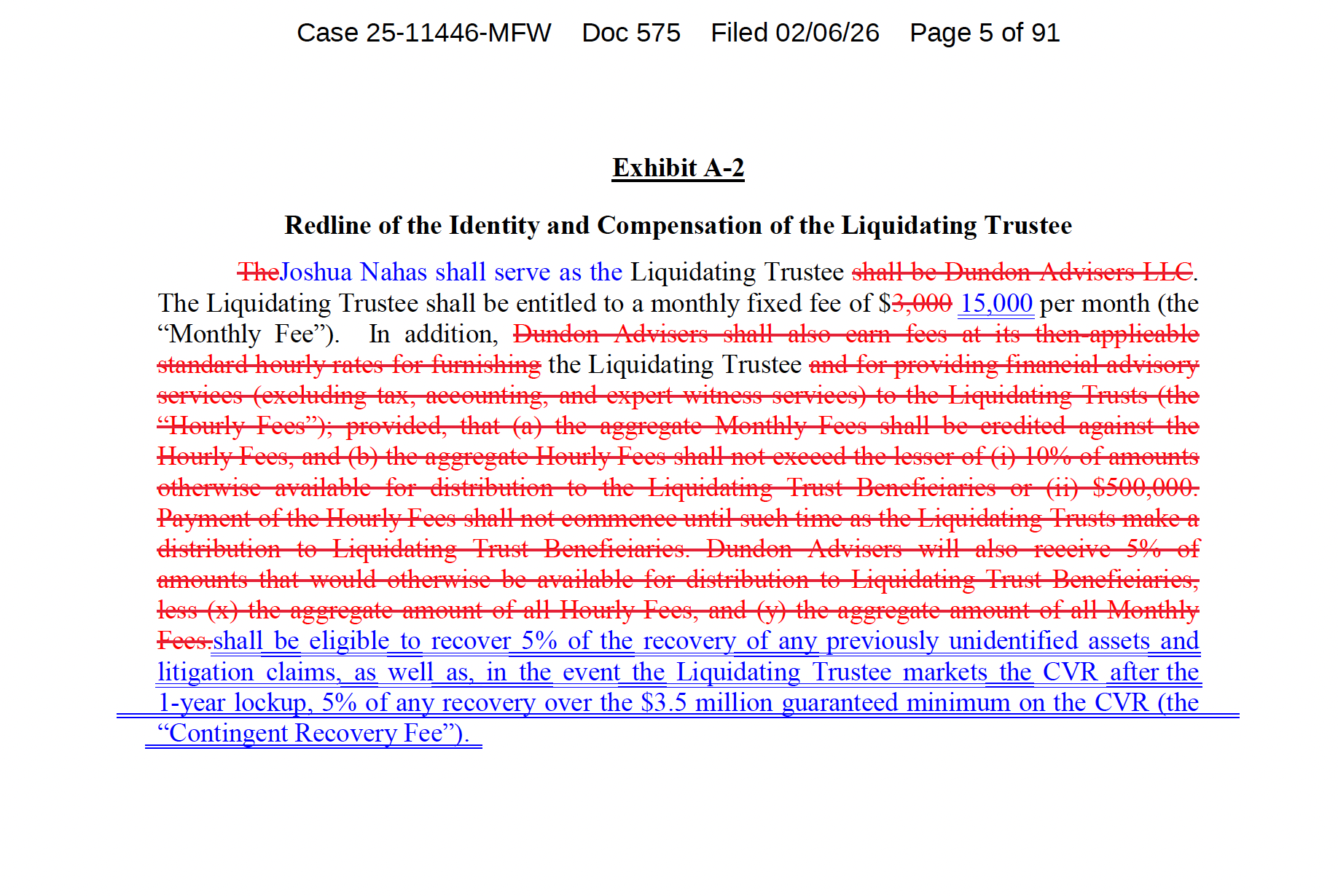

Exhibit A-2. source: U.S. Bankruptcy Court, District of Delaware. Case 25-11446-MFW Doc 575 Filed 02/06/26

When the Liquidating Trust was sold as a vehicle “for the benefit of creditors,” the headline concessions all pointed in the same noble direction: Axar funds the wind-down, steps back from a huge deficiency claim, and the estate gets a clean, orderly process instead of a bonfire of competing lawsuits. On paper, everyone moves toward closure.

Inside the trust documents, though, an interesting deal takes shape. According to the confirmed plan and Liquidating Trust Agreement filed at Docket 575 in Case 25-11446-MFW, the Liquidating Trustee’s fixed fee doesn’t just tick up—it jumps from $3,000 a month to a $15,000 monthly retainer, on top of hourly billing and contingent upside tied to new recoveries. The person who controls which claims live or die, when to settle, and how aggressively to litigate is now one of the most expensive fixed costs in a structure ostensibly built to get as much money as possible back to unpaid creditors.

Joshua Nahas: Bankruptcy Veteran as the New Trustee

Joshua Nahas, CIRA (25+ years), ex-distressed debt PM, creditor committee veteran (Caesars, Lehman, PG&E). Now Brooklyn Mirage Liquidating Trustee—collecting $15K/month while controlling all claims.

Those same documents make Joshua Nahas of Dundon Advisers LLC, as Liquidating Trustee, the single most powerful actor in the estate’s afterlife—paid first, indemnified heavily, and armed with broad discretion over which claims to pursue or drop. Perfectly legal. The question: are unsecured creditors effectively represented, or just nominally protected?

The court called the Global Settlement (D.I. 372) "remarkable": $1.05M upfront + $750K annually x3 years. Whether those payments hold as Nahas's $15K/month accumulates remains the structural tension.

From the outside, it is hard not to read the incentives a certain way. On one level, the justification is standard: complex post-confirmation litigation needs a seasoned professional. You pay for experience and for someone willing to sit in the blast radius of angry creditors, opportunistic defendants, and years of procedural grind. A higher retainer, plus upside, is framed as the price of getting a serious player to take the keys.

But look at the incentives from Axar’s side of the table. As the buyer and settlement counterparty, Axar’s interest is in locking in its bargain and containing litigation risk around the deal, the CVR, and any residual claims that might claw back value it thinks it has already paid for. A trustee who is well-compensated, heavily indemnified, and armed with “absolute discretion” over which causes of action to pursue can function as a stabilizer: someone who will weigh risk, optics, and timing in a way that won’t casually blow up a global settlement. If you assume that’s part of the job, $15,000 a month isn’t an indulgence; it may align with settlement stability.

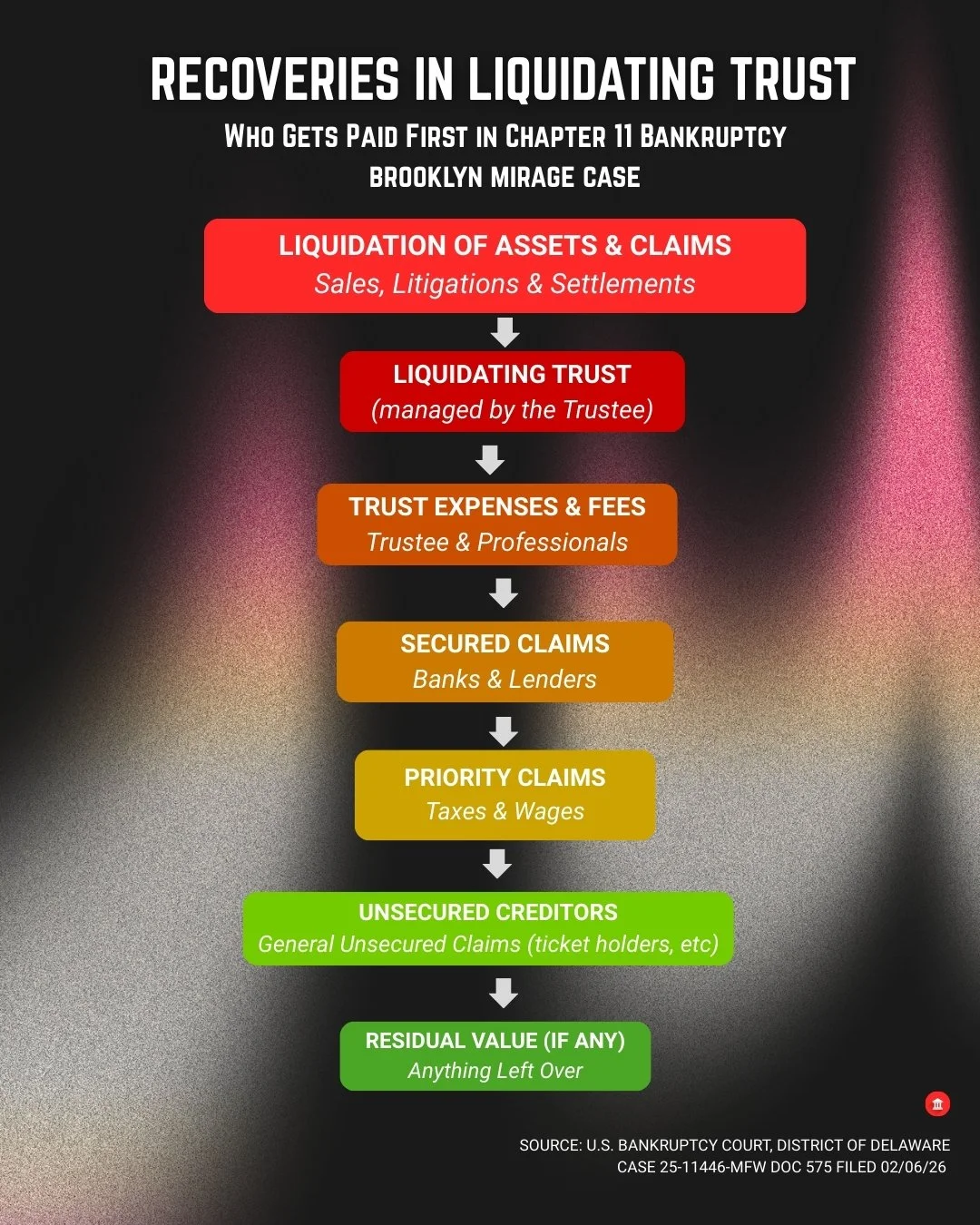

Brooklyn Mirage Chapter 11: Recoveries in Liquidating Trust.

source: U.S. Bankruptcy Court, District of Delaware. Case 25-11446-MFW Doc 575 Filed 02/06/26

From the creditors' side, the math looks harsher. Every month the case drags on, the first $15,000 comes off the top before a single dollar flows to vendors, ex-employees, contractors, or artists still owed money from the venue's pre-petition days. Layer in hourly fees and contingency percentages and the trust prioritizes professional overhead before broader recoveries. "That's a standard practice," legal counsel told Unmixed. "It's considered an administrative fee which gets paid out first." The structure raises questions about trustee alignment with secured versus unsecured creditor interests.

No filing openly says, "this trustee will protect Axar." The documents speak in neutral terms: fiduciary duty, best interests of the trust, maximization of net recoveries. A compensated trustee with discretion over litigation and disclosure creates incentives that may prioritize settlement stability. For the people at the bottom of the waterfall, it can feel like paying for professional overhead.

Lender Control and Asset Transfers

Axar provided $45.8 million in DIP financing and secured court approval for their $110 million credit bid through affiliate AG Acquisition 1 LLC on October 22 despite creditor objections. Merchant cash advance lenders sued afterward (Bloomberg Law first reported), alleging misrepresentations about Avant Gardner's financial condition and DOB issues during 2024-early '25 extensions. They sought to unwind the sale, citing management decisions, but Judge Mary F. Walrath approved it with a "remarkable settlement" providing value to unsecured creditors. Axar transferred assets by early January 2026 to Dubai's FIVE Holdings (Pacha parent) following settlements—positioning the site for summer relaunch as "Pacha New York."

The Judge's Threshold

The judge's role sits in the background of all this. The plan, the trust, and the fee framework have already been confirmed as proposed in "good faith" and in the "best interests" of the estate. Courts routinely approve negotiated fee structures in complex reorganizations; this case is not an outlier so much as an unusually visible example. That doesn't mean the court endorsed every future exercise of the trustee's discretion; it means, given the record and the options on the table, this package cleared the threshold for approval. Whether that calculus still looks acceptable as monthly retainers stack up and unsecured recoveries thin out is a question that usually surfaces only if someone has the money and appetite to challenge fees later.

Unmixed has reached out to Gary Richards, CEO of Avant Gardner and public face of Brooklyn Mirage, for comment on the liquidating trust structure, the trustee compensation terms, and what this means for unsecured creditors still awaiting recovery. No response was received by press time.

For now, what you can say with certainty is this: a trust that exists, in theory, to pay creditors has elevated the person in charge of that mission into one of its primary beneficiaries. The open question—what this piece leaves hanging—is whether that is a necessary cost of order in a broken system, or proof that in Chapter 11, the people doing the cleaning always get paid before the people left holding the bill.

Source

— U.S. Bankruptcy Court, District of Delaware. Case No. 25-11446

related:

Sold in the Headlines, Not in Court: Brooklyn Mirage’s Pacha Deal Blows Up in BankruptcyBrooklyn Mirage’s Chapter 11: What’s in the Committee’s 14-Point ObjectionPacha New York: What the Press Release Won’t Say Out LoudBrooklyn Mirage Bankruptcy: $90K 'Services Provided' to Firm in Carone Corruption ProbeBrief Timeline prior to Chaper 11

City Hall Connections

2014: Eric Adams becomes Brooklyn Borough President; Ingrid Lewis-Martin serves as his deputy and maintains an active working relationship with attorney Frank Carone on DOB matters, including for Avant Gardner owner Jürgen “Billy” Bildstein.

Carone represented Bildstein and other Brooklyn clients while remaining a close Adams ally; City Hall has said ethics rules were followed.

Fabien Levy, then in the Adams press shop and now deputy mayor, publicly praised Avant Gardner, and Hell Gate NYC reporting describes an email sent on the venue’s behalf to the governor’s office.

No bankruptcy filings to date link these political relationships to the 2025 DOB enforcement actions, TCO revocation, or later inspection process.

Axar Capital Timeline

2021: Axar begins secured lending to Avant Gardner affiliates, taking senior creditor status over the Brooklyn Mirage/Avant Gardner complex.

2022: Bildstein acquires Made Event (Electric Zoo’s parent) from Axar for about 15 million dollars; Axar remains a key creditor and retains leverage via remaining claims.

By September 2023, after Electric Zoo’s operational failures, Axar increases involvement and extends a senior secured term loan that grows from roughly 121 million dollars to about 143.6 million dollars, plus 20–22.6 million dollars in “protective advances” by 2025, to fund Brooklyn Mirage renovations under DOB scrutiny.

April 28, 2025: DOB issues TCO OCO-073885, then revokes it in late April before a final safety inspection; a subsequent DOB statement and former Commissioner James Oddo cite structural and safety issues, not just paperwork gaps.

April 30–May 1, 2025: Construction permits go “on hold,” forcing an operational shutdown even as tickets are sold for the season.

June 2025: Axar principal Andrew Axelrod engages officials on permit and construction status amid rising costs and public 2026 reopening messaging.

August 2025: AGDP Holding files Chapter 11 in Delaware (Case No. 25-11446), disclosing about 155.3 million dollars in secured debt, including roughly 11.9 million dollars junior to LiveStyle Inc.

Post-Sale Control & Compensation

Axar ultimately acquires the assets via a 110-million-dollar credit bid and settlement package, then installs a board where its representatives Gary Richards and Hooman Yazhari hold an effective 2-to-1 majority.

Publicly filed plan/board documents describe Yazhari continuing as a director at about 35,000 dollars per month and Richards in a senior executive role at roughly 650,000 dollars per year.

The estate moves into a liquidating trust structure where trustee and professional fees—including Joshua Nahas’s 15,000-dollar monthly retainer—are paid ahead of most creditor recoveries.