How Brooklyn Mirage Became a Financial Asset: Inside the Bankruptcy and $120M Axar Loan

Financial Distress, Bankruptcy Governance, and Asset Control in the Nightlife Economy

by Nina K.Malik

Brooklyn Mirage. 2025

The Nightlife Story You Thought You Knew

On a bustling morning in a Delaware bankruptcy courtroom, the future of Brooklyn’s largest independent nightclub was reduced to a single word in a stack of legal filings: An asset.

That change in vocabulary was easy to miss. But it marked the point at which one of the city’s most visible independent venues stopped being discussed as culture and began to be processed as distressed property: a web of leases, debt obligations, contractor claims, construction risk, and competing rights to whatever value remained.

The public version of the story sounded simpler. Mirage had run into trouble. Construction delays. Safety scrutiny. A chaotic reopening. Then, eventually, bankruptcy.

In nightlife circles, the explanation circulated through group chats, Instagram comments, and the usual Reddit autopsies.

For months, the Mirage bankruptcy kept resurfacing in headlines, each new filing revealing another piece of a venue whose problems were larger than any single failed opening weekend.

But the documents prove the collapse was not the result of one crisis. It was the result of several pressures building at once.

Even before the bankruptcy filing became public, the company behind Mirage was already navigating a severe internal cash shortage. Weekly executive reports tracked liquidity with growing urgency. Construction contractors began filing liens against the property as payments slowed.

Lenders injected capital in carefully staged tranches while a major redevelopment project continued advancing through engineering and regulatory review.

Billy Bildstein remained the founder and controlling owner of the entities behind Avant Gardner and Brooklyn Mirage. At the same time, Axar Capital – the venue’s senior secured lender – had become deeply embedded in the company’s capital structure as financial pressure mounted.

To the public, Mirage still looked like a venue trying to reopen. Inside the company, it increasingly looked like a business trying to buy time.

And by the time the court approved the transfer of the venue complex through what was presented as a competitive sale, much of the transformation had already taken place.

Reporting by The Wall Street Journalrevealed that Axar Capital had extended roughly $120 million in loans to the Mirage over several years, eventually converting that debt into ownership through the bankruptcy process.

But that account captures only the broad outline of the financial story.

The documents surrounding the bankruptcy – internal reporting, contractor liens, and regulatory filings reveal a more complicated sequence of financial pressures that unfolded long before the venue formally entered Chapter 11.

The First Alarm Did Not Come From the City

Public narratives tend to search for visible causes. In the Mirage story, that meant construction failures, city scrutiny, and safety concerns.

But the earliest unmistakable warning signs appear somewhere less theatrical and far more consequential:

cash-flow reporting.

Internal board reports circulated among Avant Gardner leadership throughout 2025 show the company increasingly preoccupied with one problem: liquidity survival.

Executives tracked revenue performance not as a long-term growth indicator but as a near-term survival metric. Weekly updates repeatedly emphasized the need to stabilize cash flow, reduce operating expenses, and improve ticket sales performance across upcoming events.

One report noted that key shows over the next four weeks would determine whether financial projections could hold.

Another highlighted weaker-than-expected ticket performance from several high-profile bookings:

Peggy Gou

Subtronics

Nora En Pure

Tape B

Galantis

Inside these reports, ticket sales had taken on a different meaning.

They were becoming a test of solvency.

The company’s financial model assumed event revenue would sustain operations while a larger redevelopment project moved forward.

If ticket revenue faltered, the gap between operating costs and available cash would widen quickly.

Internal projections suggested the company required roughly $12.5 million in additional funding to achieve what executives described as a “permanent positive cash position.” In other words, the venue was already operating inside a financial gap large enough to threaten its survival.

That phrase appears repeatedly in the internal reporting.

It is the language of a company already operating in financial distress – and dependent on its senior lender, Axar Capital, to continue funding the project.

But the additional capital never fully arrived.

Mirage did not collapse suddenly.

It was gradually pushed into deeper financial distress, the kind that restructurings often require before an asset becomes transferable.

In distressed finance, this process has a familiar outcome: once the operating company weakens enough, control shifts to the parties holding the debt behind it

Running on Tranches

As cash pressure intensified, the Mirage operation moved into a financing structure common among distressed companies: staged capital injections.

The board reports reference two funding sources repeatedly.

TVT Capital had already funded approximately $6.25 million by late February.

Another $2 million tranche was scheduled for release shortly afterward.

Axar Capital had funded an initial $5 million tranche, with an additional $7.5 million contingent on performance.That funding was expected to help stabilize the company’s liquidity as the redevelopment continued.

But the additional capital did not fully materialize during the period when internal reports show the company’s cash position deteriorating.

In restructuring circles, financing structures like this are sometimes associated with what is known as “loan-to-own” pressure, where lenders, in this case Axar Capital, gain control as financial distress deepens.

For companies under stress, tranche financing functions as both lifeline and leverage. Capital arrives in phases rather than as a single investment. Each tranche requires continued confidence that management can stabilize the business long enough to justify further funding.

In theory, the structure protects lenders from excessive exposure.

In practice, it shifts the internal balance of power.

When operating survival depends on staged capital injections, management decisions begin revolving around one objective:

unlocking the next tranche.

The company was no longer pursuing growth so much as purchasing time – tranche by tranche.

Your tickets funded Mirage’s lawyer fees in Chapter 11

The board weekly reports of the Mirage calendar begins to read like a financial ledger. Tickets continued to be sold while the company was already preparing for a potential Chapter 11 filing. why? Because Those ticket revenues effectively functioned as short-term liquidity for the operating entity during a period of severe cash pressure. this is when events were evaluated not only for attendance projections but for their immediate impact on liquidity.

Underperforming shows triggered rapid internal adjustments. On-sale timelines shifted. Marketing strategies changed. Some events were re-announced with new promotional assets designed to boost ticket demand. Executives discussed adding second dates to increase sellable capacity. Other shows were reconsidered entirely.

These tactics are not unusual in live events, but what made the language notable was the context.

Ticket revenue was no longer simply the engine of profitability.

It had become the mechanism through which the company hoped to stabilize its financial position.

Josh Wyatt was fired in May, at this time company has an excellent knowledge that they are driving straight into the bankruptcy, so the question is, why did they not stop selling tickets, if they knew they were not going to open their doors that season? Were they collecting your money and calling it a ‘gofundme’ but without the knowledge of the ticket holders?

Source: LIRR review letter, NYC Department of Buildings filing.

The Redevelopment and Vendor timelines

While internal reports warned about cash pressure, a major redevelopment project tied to the Mirage complex continued progressing.

Here, the underlying issue was structural.

The venue required substantial rebuilding, including sections around the main stage that had already drawn safety concerns.

Source: LIRR review, NYC Department of Buildings filing.

Board updates referenced construction milestones: materials shipped, landlord amendments negotiated, environmental pile testing underway.

Externally, the redevelopment generated a dense regulatory trail.

New York Department of Buildings filings referenced structural stability inspections and demolition oversight. A licensed special inspector was assigned to monitor structural conditions.

The project also intersected with nearby freight rail infrastructure.

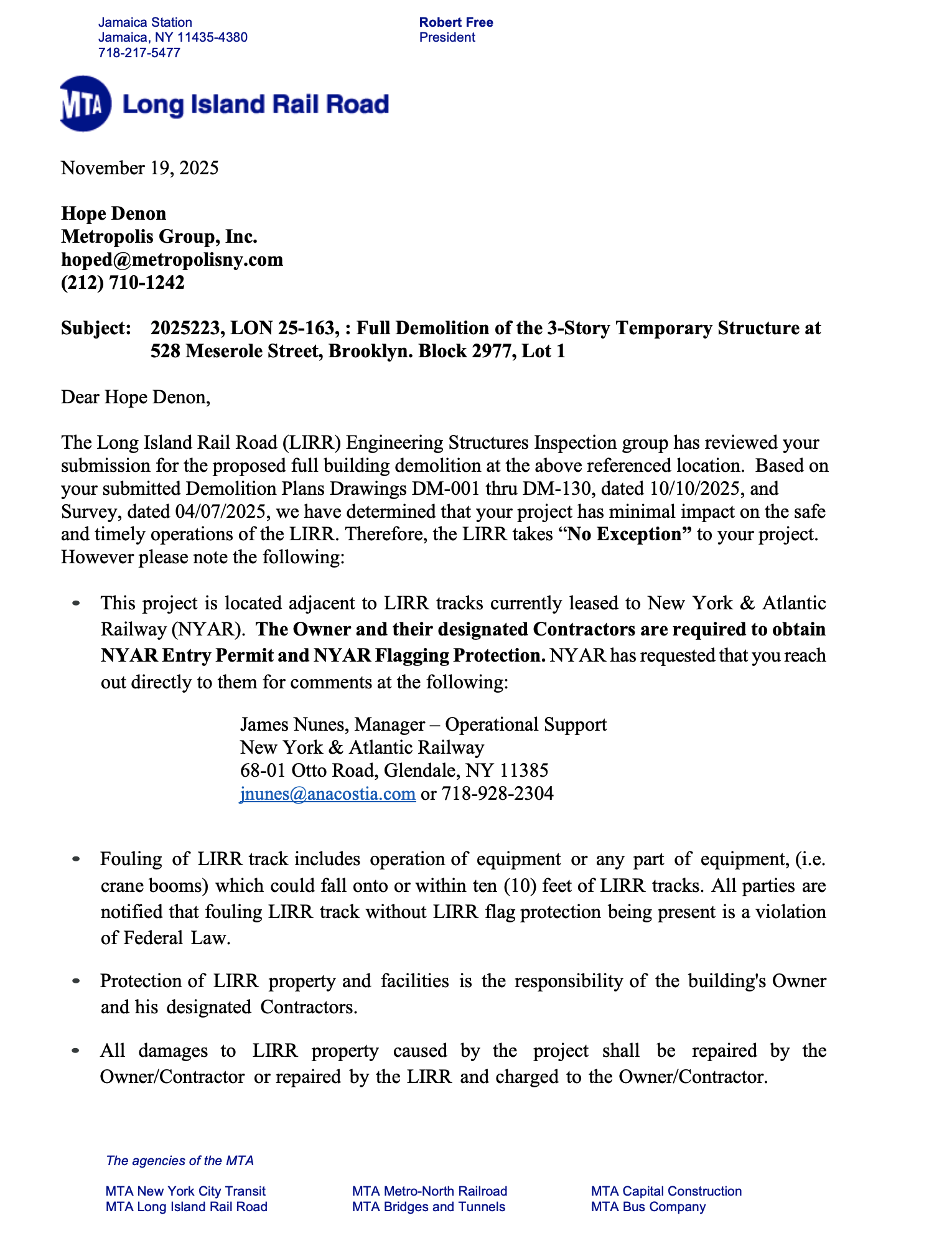

The Mirage complex sits adjacent to tracks connected to Long Island Rail Road infrastructure and New York & Atlantic Railway freight operations.

In November 2025, the Long Island Rail Road - LIRR -issued a review of demolition plans affecting structures near the rail corridor.

The response was brief:

“No Exception.”

Meaning the railroad found no objection under the submitted safety conditions.

But the review confirmed the scale of the redevelopment.

This was not routine renovation paperwork.

It was the documentation of a major construction project unfolding while the operating company itself was running out of financial room.

At this time, vendors begin adjusting their behavior. Internal reports warned that contractors might slow work because payments were falling behind.In construction, timing is everything.

When payments slow? you guessed it - crews slow.

Documentation increases and legal protections activate.

In the Mirage case, those protections appeared as mechanics’ liens - for unpaid contractor work - filed against the property.

Heini LLC – approximately $2.35 million

McAlpine Contracting – roughly $788,000

BrownTech – about $420,000

Herc Rentals – roughly $273,000

Telecom Infrastructure Corp – around $187,000

Cid Maintenance Corp – approximately $202,000

The Lease at the Center of Everything

For fans, the Mirage is a venue. For bankruptcy lawyers, it is something more technical: a leasehold tied to valuable real estate.

In distressed asset cases, the ability to assume and assign a lease can determine whether a venue survives or disappears.

The March stipulation approved in the Delaware bankruptcy case focuses heavily on the mechanics required to transfer the Mirage lease to a new operator.

Bankruptcy law requires that before a lease can be assigned, certain outstanding obligations must be taken care of.

The schedule attached to the agreement lists approximately $1.34 million in cure costs.

These include unpaid rent, legal expenses, parking rent obligations, environmental penalties, and other contractual liabilities tied to the property.

Another section addresses a previously established escrow account.

During an earlier refinancing transaction, the landlord deposited roughly $957,000 into escrow to account for potential lien exposure.

Under the stipulation, the purchaser reimburses the landlord and assumes control of the escrow account.

The practical effect is straightforward: The landlord is reimbursed , outstanding obligations are neutralized and the lease becomes transferable again.

Without that legal plumbing, the Mirage complex could not easily change hands.

But Mirage does not occupy a single property. The complex spans multiple addresses in the area, with one of their backoffices located at 100 Bogart where, according to the owner, a separate court action is determining the fate of the lease and its costs.

In Bankruptcy, Claims Also Change Hands

Another layer of the bankruptcy involves the trading of creditor claims.

One of the largest claims tied to the Mirage case originated with LiveStyle - who’s the main promoter of Electric Zoo festival.

The company initially asserted a secured claim of approximately $11.95 million.

Through negotiation, the claim was reduced and reclassified as an unsecured claim of roughly $9.95 million.

Later, the claim was transferred to an investment entity known as Bradford Capital.

This type of claim trading is a common feature of large bankruptcies. Distressed debt investors purchase claims from original creditors, often at a discount, hoping to profit from the eventual restructuring outcome. Trading ‘invisible money’, or what they themselves call, ‘future receivables’ is one of the favorite things of financiers of this century.

Brooklyn Mirage. May 2024

The Auction Question

Bankruptcy asset sales are designed to maximize value through open competition.

Multiple prospective bidders interviewed for this investigation say that competition may not have been as open as the process implied.

Several individuals who explored submitting bids told Unmixed they encountered barriers that discouraged participation.

Some describe limited access to the process.

Others say they were unable to obtain sufficient information to prepare meaningful offers.

At least one potential bidder alleges they were misled about the nature of the opportunity.

Those claims remain disputed, and individuals connected to the process deny wrongdoing.

But the accounts introduce a central question that continues to shape the Mirage story.

If the venue complex was sold through a competitive bankruptcy auction, how many bidders were actually able to participate?

A Pattern, perhaps?

Taken on their own, the pieces of the Mirage story seem almost ordinary. A nightclub under financial strain. A construction project bogged down in disputes. A restructuring meant to clean up the balance sheet. Nothing unusual – until you start placing the documents side by side. Then a larger pattern emerges: cash reserves running thin months before bankruptcy, lenders wiring money in cautious tranches, construction advancing even as vendor payments stalled. Liens began stacking up, debts changed hands between investors, and lease terms quietly shifted – all steps that, together, prepared the property for its final transfer.

A distressed nightlife venue becomes a reorganized real estate asset.

The Mirage collapse is sure as hell not just a nightlife story.

It is a perfect case study in how cultural infrastructure moves through financial systems when operating companies fail.

Nightclubs are often treated as ephemeral spaces defined by artists, crowds, and nightlife culture.

But behind those experiences sits a complicated network of leases, lenders, contractors, investors, and regulatory agencies.

When a venue collapses financially, its future is shaped not only by promoters and DJs but by the legal and financial structures that govern distressed assets.

Sometimes the transition occurs through a transparent auction.

Sometimes it unfolds through negotiations and stipulations that gradually reassign risk and control.

Either way, the music eventually returns.

What stays less visible is the financial choreography that determined who is controlling the room now - Dubai bank sponsored luxury brand “PACHA” under FIVE holdings corporation trying to expand worldwide to secure their assets in times of active conflict and the ongoing war in middle East.

Source: LIRR review, NYC Department of Buildings filing.

Let’s talk Myths..

Nightlife culture tends to frame venues as creative ecosystems.

Clubs are imagined as stages for artists and communities. Their rise and fall is narrated through music, promoters, cultural trends, and lately social media presence. YIKES

But the Mirage case illustrates something even less romantic than this.

Large venues operate inside financial structures that increasingly resemble those governing hotels, casinos, and sports arenas.

They are assets. When the operating company falters, control moves toward those holding the financial leverage behind the scenes - like Axar Capital in Mirage’s story.

Billy Bildstein is avoiding press, detaching himself, but without his knowledge, we doubt Axar would achieve such goals of running the venue on tranches and driving it to Delaware bankruptcy court.

Final Observation

Brooklyn Mirage aka Avant Garner was a symbol or ‘anything is possible’, truly a mirage in the district of warehouses surrounded by trucks and railways around it. Chapter 11 showed us its darker side. The venues may look like cultural spaces. Yet increasingly, they behave like financial assets.

Nightlife is often described as culture.

The Mirage shows how quickly culture becomes collateral when the balance sheet collapses.

The dance floor won’t feel the same when the lights come back on. The difference won’t be visible at first - maybe not ever, at least not to everyone. The FiDi finance bros and tech bros drifting between New York’s other nightspots will still find comfort in overpriced tickets and bottle-service theatrics - girls in bikinis waving sparklers over a thousand-dollar Don Julio. But behind that sparkle, the room’s economics will have shifted. And while it might not touch you, my dear bros, it will touch the rest of us: in who gets booked, and which artists quietly become “unfeasible.” Large venues increasingly depend not just on ticket sales but on high-margin table service, corporate partnerships, and financial backers expecting predictable returns. When those pressures rise, who gets booked changes with them. The result is a drastic transformation of nightlife culture itself.

If the industry keeps expanding – projected to double in market value in the coming years – yet artists, venues, and independent promoters all say the margins are shrinking, the question becomes unavoidable:

Where is the money actually going?

related:

Brooklyn Mirage Bankruptcy: What Weekly Updates Knew – and Who Was Briefed on Them

Brooklyn Mirage Bankruptcy Plan Fast-Tracked in 17-Minute Hearing

Brooklyn Mirage Bankruptcy: When the Trustee Gets Paid First

Sold in the Headlines, Not in Court: Brooklyn Mirage’s Pacha Deal Blows Up in Bankruptcy

Brooklyn Mirage’s Chapter 11: What’s in the Committee’s 14-Point Objection

Pacha New York: What the Press Release Won’t Say Out Loud

Brooklyn Mirage Bankruptcy: $90K 'Services Provided' to Firm in Carone Corruption Probe